What is a Provident Fund (PF)?

A Provident Fund (PF) is a government-backed retirement savings scheme designed to provide financial security to individuals after retirement or during specific circumstances like unemployment or emergencies.

In India, PF accounts are primarily managed under two major schemes:

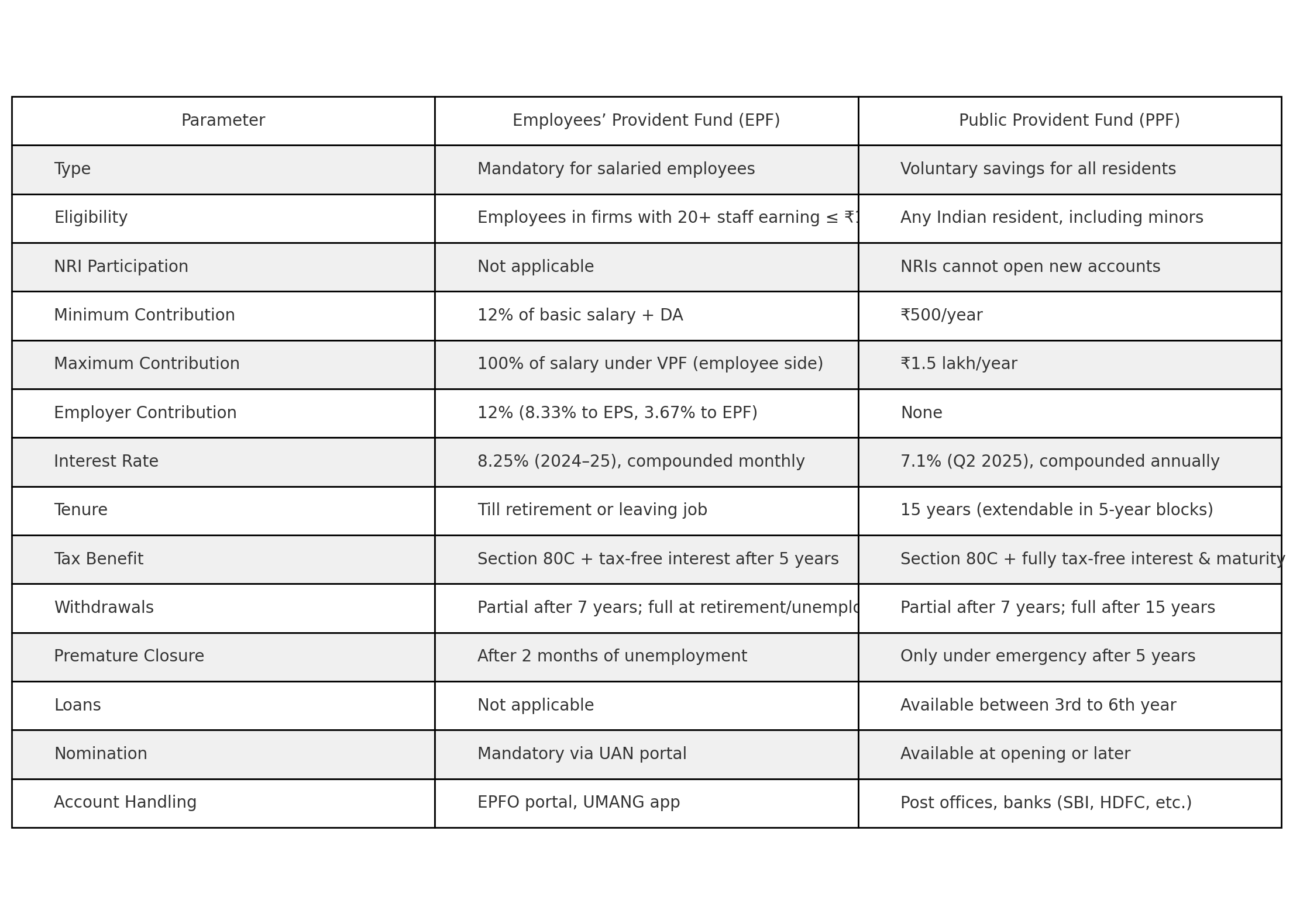

- Employees’ Provident Fund (EPF): For salaried employees in organizations with 20 or more employees, governed by the Employees’ Provident Fund Organisation (EPFO) under the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952.

- Public Provident Fund (PPF): A voluntary long-term savings scheme open to all Indian citizens, managed by the National Savings Institute under the Public Provident Fund Act, 1968.

- Other types include the Seamen’s Provident Fund (SPF) for merchant navy workers and Recognized Provident Funds (RPF) managed by private trusts.

Employees’ Provident Fund (EPF)

- Overview: A mandatory savings scheme for salaried employees in organizations covered under the EPF & MP Act, 1952. Both employee and employer contribute to the fund, which accumulates with interest for retirement or specific withdrawals.

- Eligibility: Mandatory for employees in organizations with 20+ employees if their basic salary + dearness allowance is up to ₹15,000/month.

- Employees earning above ₹15,000 can join voluntarily with employer consent under para 26(6) of the EPF Scheme.

- No age restriction for EPF membership, but pension scheme membership stops at age 58.

- Contributions: Employee Contribution: 12% of basic salary + dearness allowance (DA). Employer Contribution: 12% of basic salary + DA, split as: 8.33% to the Employees’ Pension Scheme (EPS) (capped at ₹15,000) and 3.67% to the EPF account.

- Additional voluntary contributions can be made via the Voluntary Provident Fund (VPF), up to 100% of salary, but employer contributions remain capped at 12%.

- Interest Rate: Set annually by the government, currently at 8.25% for 2024-25 (compounded monthly). For example, an 8.25% annual rate translates to a monthly rate of 0.69% (8.25/12).

- Universal Account Number (UAN): A unique 12-digit identifier linking all EPF accounts across employers, simplifying balance checks, transfers, and withdrawals.

- PF Account Number: A unique identifier for each employer’s PF account (e.g., MH/BAN/1234567/000/1234), used alongside UAN for tracking contributions.

- Tax Benefits: Contributions are deductible under Section 80C (up to ₹1.5 lakh), and interest/accumulated amount is tax-free if withdrawn after 5 years of continuous service. Withdrawals before 5 years may be taxable.

- Inoperative Accounts: Accounts with no contributions for 3 years (post-retirement, unemployment, or migration) become inoperative but can still be accessed via UAN.

- Accessing EPF Balance: Online (EPFO Portal): Log in to epfindia.gov.in or the Unified Member Portal (passbook.epfindia.gov.in) using UAN and password to view the passbook (available 6 hours after registration).

- UMANG App: Check balance, raise claims, or apply for UAN using the app.

- SMS: Send “EPFOHO UAN [language code]” (e.g., ENG for English) to 7738299899 from a registered mobile number or Missed Call: Dial 9966044425 from a registered mobile for balance details.

- Exempted Trusts: For employees under private trusts, balance details are available via company HR, salary slips, or internal portals, not the EPFO portal.

- Withdrawals:

- Full Withdrawal: Allowed at retirement (age 58) or after 2 months of unemployment (100% of corpus). Up to 75% can be withdrawn after 1 month of unemployment.

- Partial Withdrawal: Permitted for specific purposes (e.g., medical emergencies, education, home purchase) after 7 years of contributions, subject to limits (e.g., 90% of corpus at age 54).

- Forms: Form 19 (final settlement), Form 31 (partial withdrawal), Form 10C (pension withdrawal).

- Processing Time: Claims typically settle in 15-20 days after employer approval.

- Transfers: Use Form 13 for online transfer of EPF balance to a new employer via the UAN portal.

- Nomination: E-nomination via the UAN portal ensures funds go to nominees in case of the member’s demise.

- Grievances: Register complaints online via the EPFO portal or UMANG app for issues like delayed claims or incorrect balances.

Public Provident Fund (PPF)

- Overview: A voluntary, government-backed savings scheme open to all Indian citizens for long-term wealth creation, offering assured returns and tax benefits.

- Eligibility: Any Indian resident (salaried, self-employed, or student). Parents/guardians can open accounts for minors.

- Non-Resident Indians (NRIs) and Hindu Undivided Families (HUFs) cannot open new PPF accounts, but existing accounts can continue.

- Contributions: Minimum: ₹500 per financial year. Maximum: ₹1.5 lakh per financial year (combined limit for self and minor accounts). Deposits can be made in lump sums or up to 12 installments annually.

- Interest Rate: Set quarterly by the government, currently 7.1% for Q2 2025 (tax-free, compounded annually).

- Tenure: 15 years, extendable in 5-year blocks with or without contributions.

- Tax Benefits: Contributions qualify for Section 80C deductions (up to ₹1.5 lakh), and interest/maturity proceeds are tax-free.

- Account Management: Can be opened at post offices, public sector banks (e.g., SBI, PNB), or private banks (e.g., HDFC, ICICI). Accounts are transferable between banks/post offices.

- Inactivity: Accounts with less than ₹500 annual contribution become discontinued but can be reactivated with a ₹50 penalty per year of default.

- Withdrawals: Partial withdrawals allowed from the 7th financial year, up to 50% of the balance at the end of the 4th preceding year or the previous year (whichever is lower), once per year.

- Premature closure not allowed before 15 years, except in cases like death or specified emergencies.

- Loans: Available from the 3rd to 6th financial year, up to 25% of the balance from the 2nd preceding year, repayable within 36 months at 2% above the PPF interest rate. Only one loan per year.

- Nomination: Available at account opening or later; multiple nominees can be added.

Other Provident Funds

- Seamen’s Provident Fund (SPF): For merchant navy workers, established under the Seamen’s Provident Fund Act, 1966. Provides retirement benefits and survivor benefits, managed by the Seamen’s Provident Fund Commissioner since July 1966.

- Recognized Provident Fund (RPF): Managed by private trusts in organizations with 20+ employees, approved by the Commissioner of Income Tax. Contributions up to 12% of salary are tax-exempt; excess contributions are taxable.

- Unrecognized Provident Fund: Rare, managed by employers without government approval; contributions are not tax-deductible, and withdrawals are fully taxable.

Benefits of PF Accounts

- Financial Security: Provides a corpus for retirement or emergencies.

- Tax Advantages: EPF and PPF offer deductions under Section 80C, and returns are tax-free under specific conditions.

- Compounding: Interest compounds annually (PPF) or monthly (EPF), boosting long-term savings.

- Flexibility: EPF allows partial withdrawals for specific needs; PPF offers loans and partial withdrawals.

- Government Backing: Both EPF and PPF are low-risk, government-supported schemes.

Practical Tips

- Activate UAN: Link Aadhaar, PAN, and bank details to the UAN portal for seamless EPF management.

- Regular Monitoring: Check EPF balances monthly via SMS/missed call; review PPF passbooks annually.

- Nomination: Set up e-nomination for EPF and PPF to ensure smooth transfer to nominees.

- Plan Withdrawals: Avoid early EPF withdrawals to maximize tax-free returns; use PPF loans for short-term needs instead of premature closure.

- Reinvestment: Post-EPF withdrawal, consider fixed deposits (e.g., Bajaj Finance at 7.3% p.a.) to grow funds further.

! Know what is EPF and PPF?")

! Know what is EPF and PPF?")

")

हिंदी में भी पढ़ें")

Comments

Write Comment