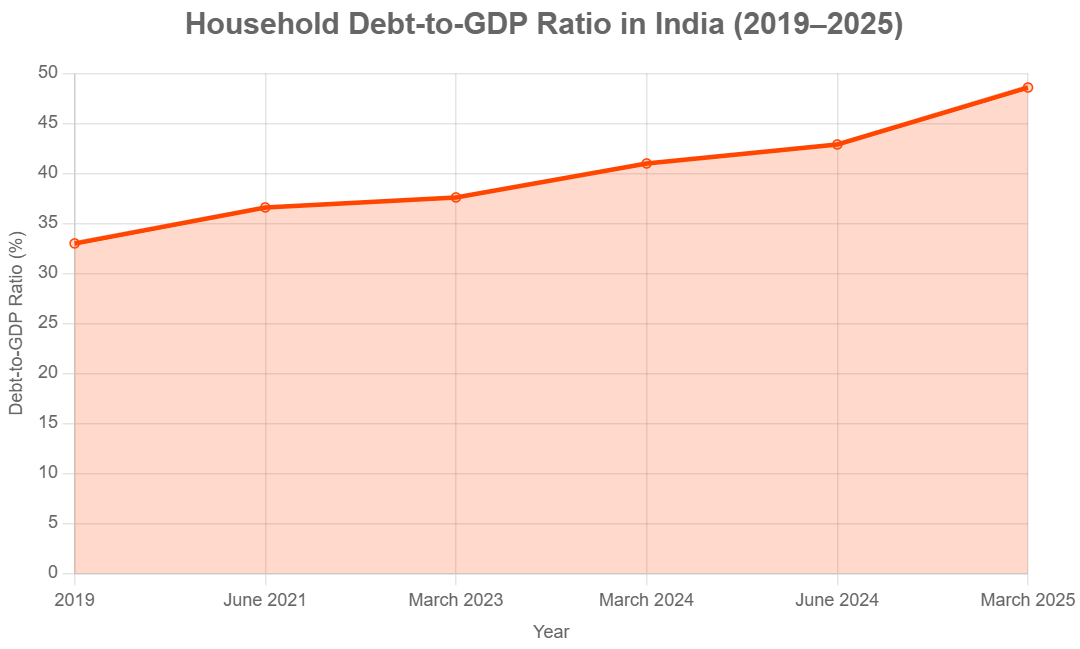

India’s household debt has become a growing concern, with recent data showing a significant rise in borrowing. By June 2024, household debt reached 42.9% of GDP, as reported by the Reserve Bank of India (RBI) in its Financial Stability Report (December 2024), a sharp increase from 37.6% in March 2023 and well above the pre-pandemic average of 33% (2015-2019).

The government’s push for financial inclusion has increased credit access, but without addressing income inequality or job creation, it risks creating a debt trap.

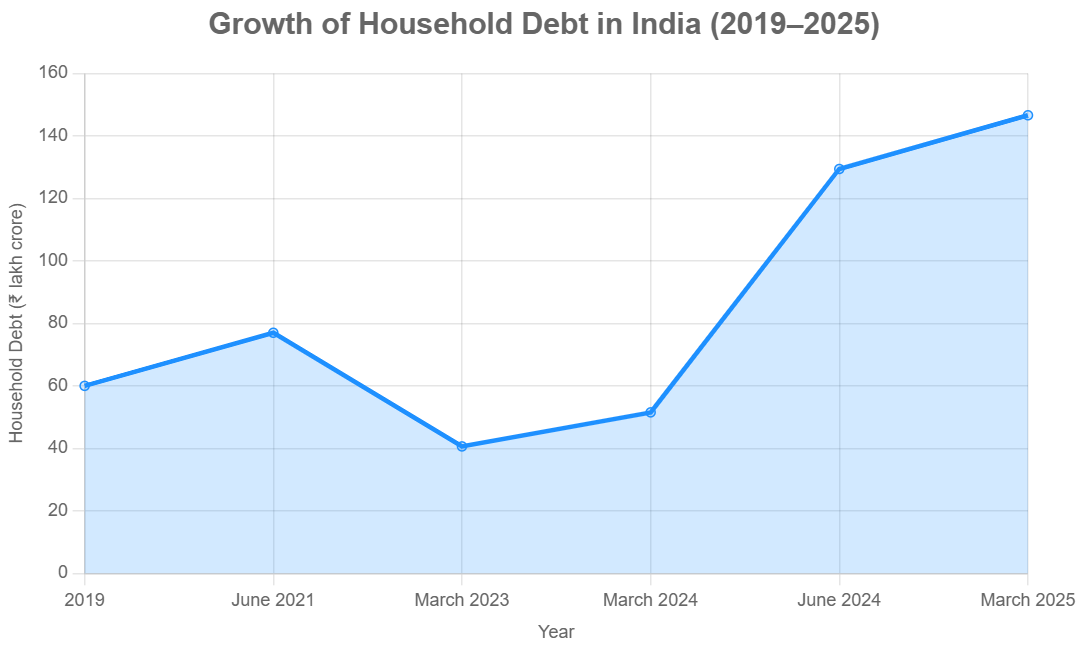

Using India’s nominal GDP for FY 2024-25, estimated at ₹331.7 lakh crore (based on Ministry of Statistics projections), this translates to ₹141.9 lakh crore in June 2024.

Personal loans, a subset of this debt, grew 24% annually between March 2023 and June 2024, totaling ₹54.9 lakh crore, or 33% of Scheduled Commercial Bank loans. The increase is largely driven by more people accessing credit (over 50% of the rise), with only a third due to higher per capita debt, reflecting financial inclusion efforts.

Super-prime borrowers, whose per capita debt rose 25% from March 2022 to June 2024, account for much of this, using 70% of their loans for asset creation (e.g., housing, vehicles), which the RBI views as financially stabilizing. India’s debt service ratio remains low at 6.5-7.0%.

Debt Service Ratio (DSR) is a measure of the share of income that households or entities use to repay debts, including both interest payments and principal repayments.A high DSR means households are spending a large part of their income repaying loans, leaving less for essential spending.

However, concerns emerge with consumption loans, which have risen since 2019, especially among sub-prime borrowers (50% of their loans are for consumption vs. 31% for super-prime). This trend, spurred by earlier RBI policies reducing risk weights on consumption loans, led to higher delinquency risks.

The RBI reversed this in November 2023, increasing risk weights, which slowed personal loan growth to 12% by January 2025. The article suggests that while the debt rise isn’t alarming due to its asset-driven nature and low debt service ratio, the growing reliance on consumption loans among riskier borrowers signals potential vulnerabilities in India’s financial stability.

Household debt in India comprises loans from banks, non-banking financial companies (NBFCs), and informal sources, including housing loans, personal loans, credit card debt, vehicle loans, consumer durable loans, and loans for agriculture, business, and education. The rapid rise since the Covid-19 pandemic is driven by structural, behavioral, and economic factors, with updated trends providing further insight:

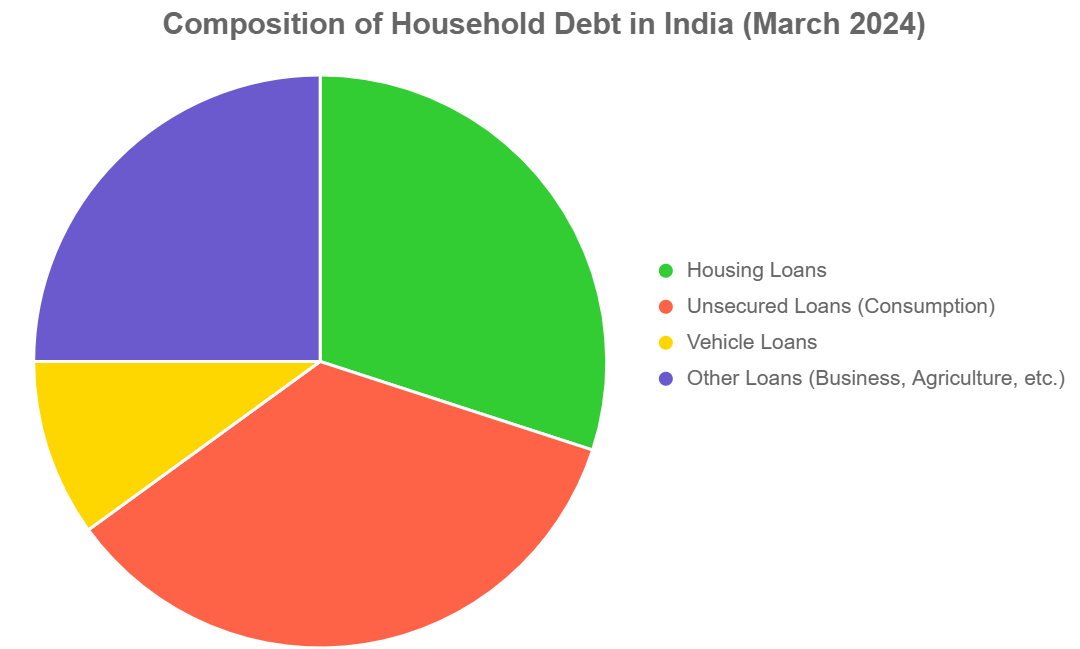

Housing loans remain the largest contributor, making up over 50% of retail loans (Care Edge Ratings, September 2024). This trend persists into 2025, with households investing in real estate as a form of long-term security, despite stagnant incomes for many. The cultural aspiration for homeownership, combined with government schemes like PMAY (Pradhan Mantri Awas Yojana), continues to fuel this debt, though rising interest rates on housing loans may strain borrowers. Care Edge Ratings notes that this debt is often productive, contributing to asset creation and supporting public infrastructure development. However, the rapid growth in mortgages—up 12.2% year-on-year in Q3 FY24—has significantly increased overall household leverage.

There has been a notable shift toward unsecured loans (e.g., personal loans, credit card debt, consumer durable loans), which grew by 18.3% year-on-year in Q3 FY24 but slowed to 12% by January 2025 after RBI interventions. Despite the slowdown, these loans remain a concern, especially for sub-prime borrowers, with 50% of their loans for consumption. Between March 2021 and March 2024, personal loans by banks grew by 75%, and NBFCs saw a 130% increase in unsecured loan portfolios.

This trend is pronounced among lower-income groups, who borrow for consumption (e.g., electronics, weddings, health emergencies), increasing delinquency risks. Microfinance delinquencies rose, with the portfolio at risk (PAR) for dues over 180 days increasing from 7.3% to 9.7% between December 2023 and December 2024, reflecting over-indebtedness, with 27% of borrowers taking new loans to repay old ones.

Post-Covid, household debt surged from 36.6% of GDP in June 2021 to 42.9% by June 2024. The pandemic eroded savings, with net financial savings dropping to a 47-year low of 5.3% of GDP in FY24, though this improved to 7.3% in H1 FY25. The earlier drop forced households to borrow for consumption, especially as income growth remained sluggish. 45% of borrowers are now sub-prime, with half their loans for daily expenses, driven by food prices doubling over the past decade and stagnant incomes. The availability of low-interest loans post-pandemic encouraged borrowing for both consumption and asset creation, such as homes and vehicles.

Banks and NBFCs aggressively expanded credit, with NBFC unsecured loan portfolios growing 130% between March 2021 and March 2024. Between March 2021 and March 2024, retail credit from NBFCs and housing finance companies grew by 70%, partly fueled by RBI’s earlier reduction of risk weights on consumption loans in 2019, though later reversed in 2023 due to rising delinquencies.

The RBI’s partial reversal of risk weights in February 2025 aims to ease lending, but this could reignite debt growth, especially in consumption loans. Microfinance institutions also contributed, with 27% of borrowers taking new loans to repay old ones, signaling over-indebtedness.

Subdued Income Growth: The sluggish income growth, especially among lower-income households (earning less than ₹5 lakh annually), has forced families to borrow for survival, exacerbating debt levels.

Income Inequality: Debt is disproportionately concentrated among lower-income and informal sector workers, who lack access to formal credit and social protection, increasing their financial stress. This debt surge impacts sectors like automobiles, consumer durables, and real estate, with FMCG firms reporting lower urban spending.

Consumption-Driven Borrowing: A growing share of loans (50% for sub-prime borrowers vs. 31% for super-prime) is for consumption rather than asset creation, raising concerns about long-term financial security.

Informal Lending: In rural areas, 31% of household loans come from informal lenders often carrying high interest rates and trapping borrowers in debt cycles, likely understating official debt figures.

The aspirational Indian consumer, particularly younger urban professionals, is increasingly borrowing to fund lifestyle expenses, education, and health emergencies. The rise in SIP contributions to ₹26,688 crore in May 2025 shows financial awareness, but many still borrow to bridge income gaps, as savings remain low at 18.4% of GDP.

The updated estimate of ₹149.9 lakh crore reflects a worrying trend, with household debt reaching 48.6% of GDP by March 2025. The RBI asserts that India’s debt levels are manageable compared to other emerging markets (42.9% vs. an average of 48.3% in June 2024), and the debt service ratio (6.5-7.0%) is among the world’s lowest.

If unchecked, this trajectory could mirror China’s, where household debt reached 62% of GDP, raising concerns about economic stability. It could also lead to a broader economic slowdown, as seen in subdued consumption challenging the narrative of a robust recovery.

Ask Anything, Know Better

November 17 BUSINESS LINE : The Reserve Bank of India could consider approving bankers’ request to lower the provisioning requirement on stage-2 loans to 1-3 per cent from proposed 5 per cent under the draft expected credit loss (ECL) guidelines, sources say. ABOUT ECL? CLICK HERE ABOUT PROVISIONING? CLICK HERE NEWS LINK

August 16 WHAT? The Reserve Bank of India (RBI) has announced a new mechanism to expedite cheque clearing, effective October 4, 2025, reducing the clearance time from the current T+1 days (up to two working days) to a few hours. The Cheque Truncation System (CTS) will transition from batch processing to continuous clearing with on-realisation-settlement, improving efficiency, reducing settlement risks, and enhancing customer experience. Implementation Phases Phase 1 (October 4, 2025 – January 2, 2026):...

August 15 WHAT? India's Stand Vindicated as Pakistan Misses IMF Loan Conditions Again.Pakistan has failed to meet three out of five key targets set by the International Monetary Fund (IMF) for the second review of its $7 billion bailout package, reinforcing India's long-standing concerns about Islamabad's poor track record in implementing IMF reforms and the potential misuse of funds. This development highlights persistent structural and fiscal weaknesses in Pakistan's economy, including revenue shortfalls and unchecked...

June 17 WHAT? The Indian government is accelerating its disinvestment drive by planning to sell up to 20% stake in five public sector banks (PSBs) within the next six months, utilizing Qualified Institutional Placement (QIP) and Offer for Sale (OFS) routes. This move aims to raise capital, improve bank governance, and ensure compliance with the Securities and Exchange Board of India’s (SEBI) minimum public shareholding (MPS) norm of 25%. The initiative is part of a broader strategy to strengthen the financial health of...

June 14 SUMMARY The article from Business Today, dated June 14, 2025, titled "Earn Rs 50 Lakh, but Save Rs 5 Lakh: Saurabh Mukherjea Warns India’s Upper-Middle-Class Is Underprepared," highlights concerns raised by Saurabh Mukherjea, Founder and CIO of Marcellus Investment Managers, about the financial habits of India’s upper-middle class. Key points Low Savings Rates: Despite earning high incomes (e.g., ₹50 lakh annually), many in the upper-middle class save only a small...

June 13 SUMMARY The Reserve Bank of India (RBI) issued new directives on June 12, 2025, to simplify the Know Your Customer (KYC) process, as reported by Business Standard. Key points Mandatory Notifications: Banks must send at least three advance written reminders before the KYC update deadline and three additional reminders, including one physical letter, if the update is not completed post-deadline. These must include clear instructions, support channels, and consequences of non-compliance. Banks are...

June 11 SUMMARY Who’s Joining? : Leading banks from France—including Crédit Agricole, Natixis, and Société Générale—along with financial institutions from the UAE, are planning to set up operations at GIFT City, India’s International Financial Services Centre Why GIFT City? : GIFT City (Gujarat International Finance Tec-City), located near Gandhinagar, stands as India’s only operational Greenfield IFSC. It offers a “foreign territory”...

June 11 Summary The government is taking proactive steps to recover ₹78,213 crore in unclaimed financial assets by: Organizing focused refund camps; Implementing standardized, digitized KYC for smoother claims; Launching a unified online platform by FY26; Ensuring timely refunds while reinforcing regulatory oversight and system resilience. These efforts aim to benefit common citizens by simplifying processes and returning long-dormant assets to their rightful owners. DETAILS As...

June 09 SUMMARY The article from Business Standard, published on June 9, 2025, titled "RBI rate cut: What it means for your money and how you should invest now," discusses the implications of a recent 25-basis-point rate cut by the Reserve Bank of India (RBI), bringing the repo rate to 6.25%. Key points Impact on Borrowing and Savings: Lower rates reduce borrowing costs, benefiting home loan and personal loan borrowers (e.g., EMIs may decrease). However, savings accounts and fixed deposits...

June 06 SUMMARY The article from The Hindu BusinessLine, published on June 6, 2025, titled "Bank deposit rate cut to boost MF inflows," discusses how a recent reduction in bank deposit rates is expected to drive increased investments into mutual funds (MFs), particularly equity schemes, due to investors seeking higher returns amid market volatility. Key points include Repo Rate Cut Impact: The Reserve Bank of India (RBI) reduced the repo rate by 50 basis points to 5.5%, following earlier cuts of 25...

Comments

Write Comment