An elasticity greater than 1 means revenues grow faster than the base (progressive taxes like income tax often score here), while less than 1 indicates sluggish response (common for regressive taxes like sales tax).

These concepts emerged in the mid-20th century amid post-WWII reconstruction, when economists like John Kenneth Galbraith and international bodies like the IMF began analyzing why some tax systems thrived while others lagged.

Elasticity gained traction in developed nations for its focus on automatic stabilizers (taxes that self-adjust to curb recessions). Buoyancy, meanwhile, became a staple in developing economies, where policy volatility is high—think India's frequent GST tweaks or the US's Tax Cuts and Jobs Act of 2017.

By the 1980s, the World Bank and IMF used them to benchmark reforms: low buoyancy in Latin America prompted base expansions, while high elasticity in Nordic countries justified progressive systems. T

oday, with climate taxes and digital levies on the rise, recent IMF studies emphasize buoyancy for long-term sustainability, noting it often exceeds elasticity due to reforms.

|

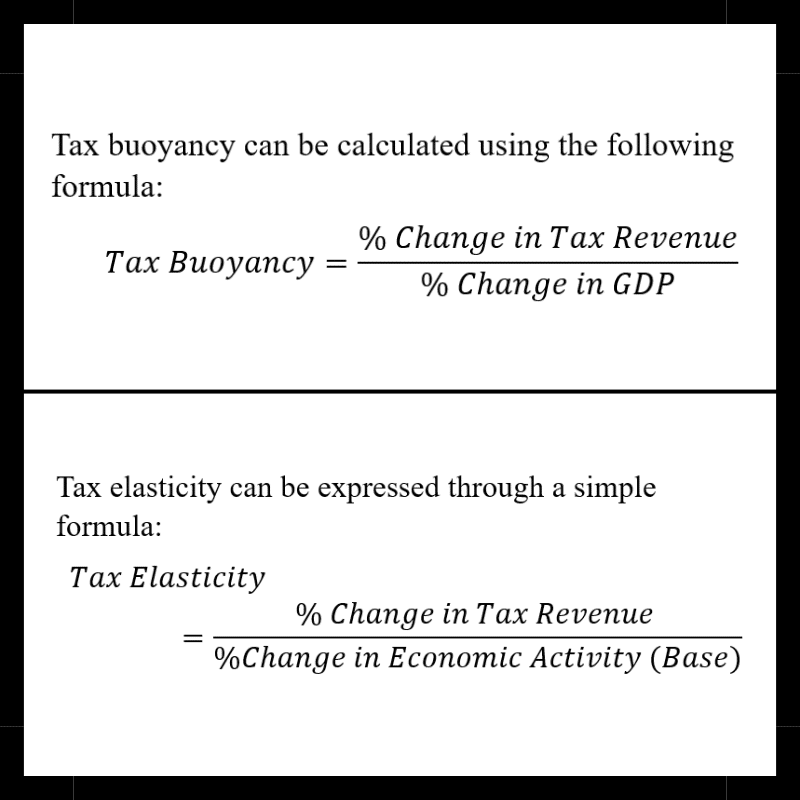

Aspect |

Tax Elasticity |

Tax Buoyancy |

|

Focus |

Response to tax base changes (e.g., income) with fixed rates |

Response to GDP changes, including policy shifts |

|

Assumptions |

No discretionary changes; holds structure constant |

Includes rate hikes, exemptions, enforcement improvements |

|

Calculation |

Adjusts for policy neutrality (e.g., via regression models) |

Direct ratio; simpler but holistic |

|

Typical Value |

Often <1 for indirect taxes; >1 for direct |

Varies; 0.8-1.2 in developing economies |

|

Use Case |

Assessing inherent progressivity |

Evaluating overall fiscal health and reform impact |

|

Limitations |

Ignores real-world tweaks; harder to measure |

Can mask structural flaws if buoyed by temporary hikes |

Ask Anything, Know Better

November 05 Introduction Have you ever wondered how we measure a country's economy? We use GDP, or Gross Domestic Product, which shows the total value of goods and services made in the whole country. But what if we zoom into smaller areas, like districts? That's where District Domestic Product (DDP) comes in. It's like GDP but for each district in a state or country. In India, DDP is gaining attention as a way to understand local economies better. This article explains what DDP is, if it's coming soon, its benefits, and why it...

September 19

June 04 WHAT? The Purchasing Managers' Index (PMI) is an economic indicator derived from monthly surveys of private sector companies. It reflects the prevailing direction of economic trends in manufacturing and services sectors. Who publishes PMI in India? Compiled by: S&P Global (formerly IHS Markit) Published for India by: S&P Global Not released by government bodies like MOSPI or RBI Types of PMI in India PMI Type Sector...

June 03 SUMMARY The article "Towards an Indian Growth Model" from The Hindu Business Line advocates for a development strategy tailored to India's unique strengths and challenges, moving beyond traditional Western economic models. Key points include Domestic Demand-Driven Growth: India's economy has been significantly propelled by domestic consumption, accounting for 64% of its GDP, surpassing figures in Europe, Japan, and China. This consumption-led approach has fostered a robust middle...

May 31 SUMMARY India has officially overtaken Japan to become the world's fourth-largest economy, marking a significant milestone in its economic ascent. Key Highlights GDP Milestone: India's nominal GDP has reached approximately $4.187 trillion for the fiscal year 2025–26, slightly surpassing Japan's $4.186 trillion, according to IMF projections. Rapid Growth: In the January–March 2025 quarter, India's economy grew by 7.4% year-on-year, exceeding expectations and...

May 30 SUMMARY India's GDP growth for the fourth quarter of FY2024–25 is projected to be around 7%, driven by robust rural demand, increased government spending, and improved agricultural output. However, the full fiscal year growth is expected to settle at approximately 6.3%, slightly below earlier estimates. Q4 FY2024–25 Growth Estimates Reuters projects 6.7% growth, citing stronger rural consumption and state expenditure, despite subdued private investment. ICRA estimates...

")

March 03 As per the recent reports, Q3 of FY 2022-23 has experienced lower growth rate than the previous quarters. GST collection is also 5% lower in February than in January. Look at the catalogues for more details.

Comments

Write Comment